If you’re juggling multiple debts and feeling the pressure of high-interest payments, you’re not alone. Many homeowners in BC are turning to debt consolidation mortgages as a smart way to simplify their finances and reduce stress — while potentially saving thousands.

What Is a Debt Consolidation Mortgage?

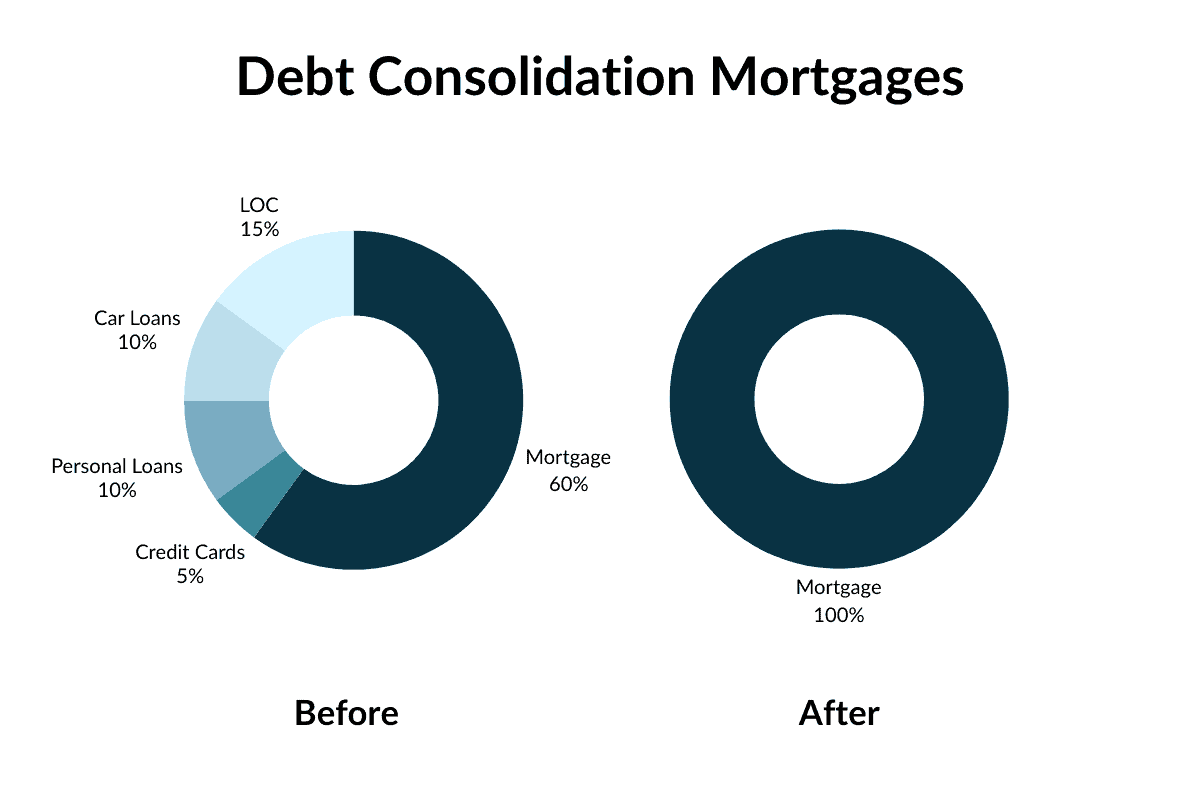

A debt consolidation mortgage allows you to combine high-interest debt — like credit cards, lines of credit, or personal loans — into your mortgage. By leveraging your home equity, you can access lower interest rates and significantly improve your monthly cash flow.

You can structure a consolidation mortgage in two ways:

- As part of your existing mortgage term

- As a standalone financing solution

Either option can help you get ahead faster and regain control of your finances.

The Benefits Are Big

- Pay off high-interest debt in 3 to 5 years — without resetting your longer-term mortgage

- Lower your monthly payments and reduce overall interest costs

- Free up cash flow for the things that matter most

- Use your home equity wisely to create more breathing room in your budget

Is This Right for You?

If you’re a homeowner in BC with equity in your property and you’re carrying high-interest debt (like credit cards or personal loans), a consolidation mortgage might be the solution. It’s designed for those looking to:

- Lower monthly payments

- Pay off debt faster

- Free up cash flow by putting their home equity to work

Curious if this could work for you? Let’s explore your options. You can book an appointment with Paul through this link or reach out via email at [email protected].

About the Author

Paul Hudson is an award-winning mortgage broker with over 20 years of experience helping homebuyers in British Columbia secure the right mortgage for their dream home.

When he’s not helping clients smart mortgage decisions, Paul is an avid snowboarder and plays in a local band in Squamish, bringing the same energy to both the slopes and the stage.